To what extent did Ancient Roman institutions facilitate the free exchange of economic resources? In his BSE Working Paper (No. 813) “The Institutions of Roman Markets,” Benito Arruñada explores the palliative methods used by Roman law to enable market exchange.

Personal vs. Impersonal Exchange

Trade plays a key role in economic growth and expanding into far-reaching markets increases the opportunities to trade. However, realizing these opportunities requires to trade impersonally, without being able to observe the characteristics of trading partners, which cause informational difficulties between purchasers and owners of property rights as they interact with all sorts of agents facilitating the transaction.

The defining conflict here is the asymmetry in the knowledge of the true ownership of the property right being exchanged—that is, the purchaser must be guaranteed that no other claimant exists in the resource. This can lead to substantive transaction costs as the asymmetry grows. Overcoming them in turn requires sophisticated and specific institutions to reduce information asymmetries in contracting while simultaneously preserving strong property rights.

Institutions for Titling Property

Achieving both goals is straightforward when the content of private contracts (such as, for instance, previous ownership transfers or representation proxies) is easy to verify. In that case, all it requires are clear adjudication rules between owners and acquirers. Acquirers are therefore secure and do not need to worry about the authority of the seller. But owners are also protected because it is they who choose the seller. And they cannot renege from their decision because the transaction produces a verifiable consequence.

Protecting third parties without damaging owners is harder when contracts remain private. Achieving both goals then requires independent registration of private contracts or property rights. Only reliable registers can ensure that owners have publicized their claims (so that acquirers can find out about them before contracting) or have consented voluntarily to a weakening of their rights with respect to innocent acquirers (so that owners cannot opportunistically renege from such consent).

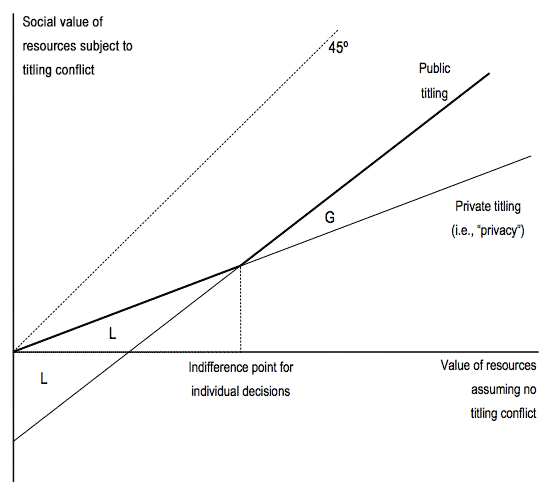

However, building registries is costly. Consider figure 1, which represents the social value of a resource (vertical axis) as a function of their theoretical value assuming no conflicting claims (horizontal axis) and using or not a registry for public titling. If owners are free to title their property (at a unit cost given by the intercept), they obtain an increase in value proportional to the value of their property. They will opt to title high-value properties while keeping low-value properties under privacy (therefore avoiding social loss L).

Social choice of institutions is then driven by the difference between the benefit from using the registry (G) and whatever fixed cost may be incurred to create it. Obviously, this difference is greater when high value assets predominate in the economy and private titling is relatively less effective. This poses a bit of a puzzle for the Roman case: in Rome, there were plenty of valuable assets that were traded at long distance, and Romans knew how registries work. But they hardly relied on them.

Where were the Roman Registries?

Arruñada indeed recounts how in the classical period of Roman law there were considerable potential gains from registries as a consequence of extensive markets, so that in terms of the figure a substantial proportion of resources lied to the right of the horizontal axis, capturing the effect of greater demand and opportunities for impersonal exchange. Evidence of a market economy in Rome abounds, e.g., in the increasing distance of trade within the Republic, the estimated 30% urbanization of Italy at the time, and the specialization of provinces in producing goods.

Moreover, Romans knew how to operate registries. In fact, the Roman province of Egypt operated vast land registries that effectively registered mortgages. And Romans also kept extensive archives for the census, and used durable media to maintain records. In fact, public and private record keeping was substantial, especially among bankers whose books the courts considered unimpeachable.

So why were registries, the prototypical institution for advancing impersonal exchange, not created?

Palliatives for Impersonal Exchange

Arruñada argues that registries would have been socially valuable and effective but for the fact that Romans made several palliative solutions relatively more effective by maximizing the use of available evidence and enacting reinforcing rules (i.e., in the figure, obtaining a steeper slope for the personal exchange line). In other words, whereas Rome lacked, by way of registries, a solution for impersonal exchange, it made up for in spades with robust institutions for personal exchange.

In property, Romans had first relied on public declarations of ownership to provide information through intricate public ceremonies of asset exchanges known as mancipatio. Among their requirements was a period of time (a grace period of sorts) to “purge” the claims of others before exchange of assets were finalized. These ceremonies, however useful in towns and small areas, became less effective when economic development lead to far-flung trading of goods. Understandably, they eventually gave way to the private conveyance of property through traditio. Further, Roman law provided public possession as access to ownership, usucapio. Initially, undisturbed possession of capital goods acquired through good faith led to ownership after two years. Over time the Praetor enhanced the path to usucapio by further protecting the good faith possessor from formal claimants, so that de facto public ownership lead to de jure ownership.

Seeming limitations of these palliatives is the apparent inability of the Roman state to implement real securities in the arena of credit-debtor relationships. Instead they relied on transferring ownership temporarily to the creditor (fiducia), but this posed serious risks to the borrower, which helps explain why they most often resorted to webs of personal sureties, especially among status equals. They were enforced through intricate social norms, some legally reinforced, that kept people to their personal obligations. In fact, real securities could have sent a negative signal: Roman culture and law regarded personal reputation as sacrosanct—so attempting to offer a security instead of your word, or even worse, no one to attest to the worth of your reputation, sent an unfavorable signal that you couldn’t be trusted.

Further, whereas early Roman law could have regarded contractual agency as incompatible with the Roman ideal of deep obligation to ones actions, Praetorial edicts eased the way to agency via the family. The vesting of rights over all members (including not only slaves but also sons) of the Roman family in the paterfamilias offered a palliative mechanism for ensuring contractual obligations when an agent (usually a slave or a son) acted on behalf of the property owner (the father). This enabled contractual specialization by bestowing the agent the ability to enact the principal’s will. Even here legal layers of protection were put in place in the event that adverse actions of the agents might jeopardize the principal into inadvertent commitment.

By using family law and social reputation (as well as formal reputational punishments via infamia and ignominia), Roman society offered palliatives to allow seemingly effective personal exchange without having formal institutions dedicated to impersonal exchange. Moreover, informal social norms were reinforced by a whole array of formal rules ensuring enforcement of personal obligations by several means, which originally included a self-help version of debtors’ prison that later evolved into debt bondage resulting from the debtors’ default, strict punishments and sophisticated allocations of liability. At a more general level, social norms protecting personal exchange were also reinforced by two sets of arrangements enabling the extended family to act as a legal entity: those allocating most decision rights to the paterfamilias; and those defining the family’s boundaries and, therefore, who could inherit and eventually act as its contractual agent, committing the family’s assets to meeting its obligations.

A Picture Emerges

Roman markets may have lacked the types of institutions that allow for impersonal exchange in modern economies, but they did not lack for palliative solutions. In particular, the enforcement of personal obligations relied not only on informal social norms but was also given substantial public support by formal law. Given this set of palliatives, the Romans may simply not have needed to incur the cost of formal titling institutions to enable the type of impersonal exchange characteristic of modern markets.

Interesting research!